Q4: Quarterly Investment Review

Independent planning for families, trustees and business owners

Markets and finances at a glance

At Oakcrest Private Office, we’re about clear, confident life plans - independent, bespoke and built to last. In this month's edition, we look at what moved markets in Q4 2025, review full-year performance statistics, and consider what to look out for in 2026. We also look at the renewed escalation in the Gulf and what geopolitical shocks like this can mean for oil, inflation and investor sentiment.

War in the Gulf: what it means for markets, and how long it might matter

Every so often, geopolitics reasserts itself in financial markets.

For most of the past year, investors have been focused on interest rates, inflation, artificial intelligence and economic growth. But occasionally the world reminds us that economics does not operate in a vacuum. Right now, that reminder is coming from the Persian Gulf.

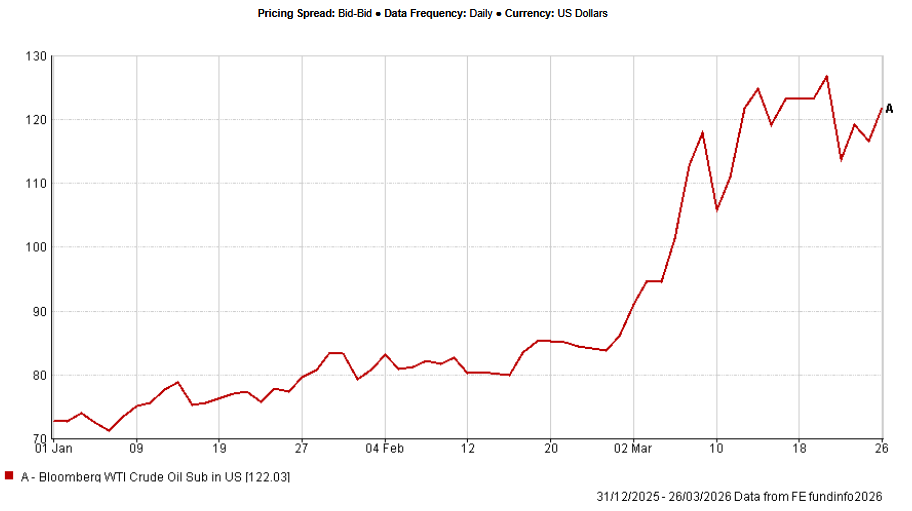

The conflict involving Iran has escalated sharply, and from a market perspective, the key issue is geography. Iran sits beside the Strait of Hormuz, the narrow shipping lane through which roughly 20% of global oil supply normally passes. If that artery becomes blocked, even temporarily, the global economy feels it almost immediately.

Oil is the market’s early warning system

Whenever tensions rise in the Middle East, oil markets tend to react first. Energy markets price in risk rapidly, often before any actual disruption occurs.

That is why the first market response to a geopolitical shock is usually seen in crude oil prices, before it feeds through into inflation expectations, bond yields and wider risk sentiment.

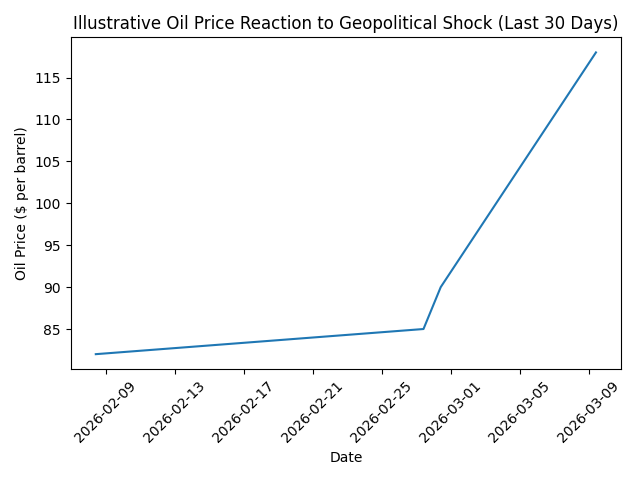

How markets typically react to geopolitical shocks

Financial markets tend to follow a recognisable pattern after geopolitical shocks. Initial volatility is often followed by a period of assessment and, eventually, normalisation.

Source: Leduc, S. and Sill, K. (2004) ‘A quantitative analysis of oil-price shocks, systematic monetary policy, and economic downturns’, Journal of Monetary Economics, 51(4), pp. 781–808.

Typical timeline

Phase 1: Shock (1–2 weeks) - markets react sharply, oil rises, and equities fall.

Phase 2: Assessment (3–8 weeks) - investors assess whether the conflict escalates.

Phase 3: Economic transmission (2–6 months) - higher energy costs begin to filter through into inflation and growth.

Phase 4: Normalisation (6–12 months) - markets gradually refocus on economic fundamentals.

Why oil prices matter for inflation

Energy costs ripple through the global economy. Rising oil prices increase transport, manufacturing and agricultural costs, and can push inflation higher. This is why markets watch oil so closely during periods of geopolitical stress: it is not just a commodity move, but a potential macroeconomic transmission channel.

What long-term investors should remember

Geopolitical shocks are unsettling, but they do not always leave a lasting mark on markets. History shows that while such episodes can trigger sharp short-term volatility, long-term investment outcomes are usually driven more by growth, earnings and policy than by the shock itself.

For now, the message is one of caution rather than panic. Oil has once again proved to be the market’s early warning system, and the latest moves are a reminder that geopolitics can still interrupt an otherwise improving macroeconomic backdrop. In the end, the duration of the shock is likely to matter more than the drama of the first headline.

Other sources:

European Central Bank (2021) Energy price developments and their contribution to euro area inflation. Economic Bulletin, Issue 3. Available at: https://www.ecb.europa.eu (Accessed: 23 March 2026).

Choi, S., Furceri, D., Loungani, P., Mishra, S. and Poplawski-Ribeiro, M. (2018) ‘Oil prices and inflation dynamics: Evidence from advanced and developing economies’, Economic Modelling, 72, pp. 45–61.

Blanchard, O.J. and Galí, J. (2007) ‘The macroeconomic effects of oil price shocks: Why are the 2000s so different from the 1970s?’, NBER Working Paper No. 13368. Available at: https://www.nber.org (Accessed: 23 March 2026).

Kilian, L. (2008) ‘The economic effects of energy price shocks’, Journal of Economic Literature, 46(4), pp. 871–909.

Q4 2025: Broadening, not just buzzing

If you only read one thing: Disinflation broadened, policy nudged easier (two Fed cuts, one BoE), and leadership started to widen beyond US mega-cap tech. Non-US markets outpaced the US over 2025; UK gilts were a notable outperformer among major bond markets; precious metals surged while oil finished the year lower at US$57/bbl (WTI).

Update (since quarter end): Since quarter end, renewed escalation in the Middle East has triggered a sharp energy shock: oil surged above US$100/bbl, with Brent touching roughly US$119 before easing after reports that G7 finance ministers would discuss a possible coordinated release of emergency reserves. The move has weighed on both equities and government bonds, as markets reprice higher inflation and greater geopolitical risk.

UK - global earners on the front foot; gilts shine

What happened: UK shares advanced again. A slightly softer pound and resilient dividends supported globally oriented blue-chips, notably in financials, mining, defence and other commodity-linked areas. Domestically exposed names were more mixed as household budgets stayed tight. Gilts outperformed major peers after a market-friendly Budget and a close BoE cut.

Our take: Income and quality did most of the heavy lifting. With the rate narrative shifting from “higher for longer” to “somewhat lower for somewhat longer,” front-end carry and roll-down were no longer theoretical, instead showing up in returns.

What we saw in positioning: A bias to high-quality UK companies with global cash flows; selective mid-caps where pricing power is credible; 1–5-year bond ladders for tidy, predictable income. With services inflation comparatively firm, index-linked gilts remained a pragmatic sleeve.

Crowd check: The UK “value” story has mindshare, but the winners tended to pair value with balance-sheet strength and cash discipline.

US - cuts delivered; breadth improving at the edges

What happened: The October and December 25 bps cuts underpinned risk appetite. Equities rose into year-end, although there was some profit-taking late on. Leadership remained concentrated in communication services and tech, but cyclicals and defensives (industrials, financials, healthcare, utilities) posted strong full-year gains; parts of tech still look fully valued versus history.

Our take: The soft-landing narrative held, but 2026 now needs earnings breadth to keep pace with price. We saw hints of broadening, but durability is the test.

What we saw in positioning: Keep owning the winners without being hostage to them; pair equity risk with short/intermediate high-quality bonds now that bonds actually pay.

If markets are wrong: A stickier-than-hoped services inflation pulse or a firmer dollar could re-tighten financial conditions and re-narrow leadership.

Europe (ex-UK) - steady as she goes

What happened: The ECB stayed in wait-and-see mode. Continental equities were firm; financials led, while steady cash-flow sectors drew interest as yields fell. Macro remained two-speed—Germany’s manufacturing stayed weak while services held up. For context, the Eurozone (MSCI EMU) returned more than 40% in 2025 (USD), comfortably ahead of the US.

Our take: With rates steadier and earnings quality improving, Europe is a stock-picker’s market - so long as global capex doesn’t stall.

What we saw in positioning: Preference for balance-sheet strength and dependable cash generation (financials, select defensives); adding exposure selectively rather than “buying the basket,” and keeping position sizes disciplined given the two-speed backdrop.

If things go the other way. Intra-EU trade still looks fragile; if demand doesn’t follow through, stock-picking beats blanket exposure.

Emerging markets & Asia - North Asia’s tech did the heavy lifting

What happened: EM outpaced DM in Q4. Korea benefited from AI-memory demand; Taiwan from semis/hardware; Chile and South Africa tracked stronger precious-metals prices; Brazil and Mexico also outperformed; China slipped late as property stress resurfaced; Saudi Arabia lagged. Across Asia ex-Japan, MSCI AC Asia ex-Japan gained ~4.3% in Q4 and ~32% in 2025 (USD), with North Asia’s tech complex (semis, hardware, data-centre infrastructure) still the engine.

Our take: EM works where capex meets earnings clarity; we leaned into supply-chain run-rates over blanket beta.

What we saw in positioning: Sensible position sizing; preference for clearly supported earnings clusters (Korea/Taiwan); a realistic, selective approach to China.

On the radar: China property headlines, US dollar drift, and metals pricing, any wobble there can ripple across EM sentiment.

How we’re positioned

Equities: Broad global exposure with a modest tilt outside the US. In the UK, global earners did the heavy lifting; selective mid-caps with genuine pricing power; trimmed single-name concentration versus earlier in 2025.

Bonds: With gilts outperforming and the BoE cutting, many kept 1–5-year ladders for carry/reinvestment discipline and nudged duration out at the margin. High-quality IG credit (EUR/GBP) remained a core income sleeve; a steeper US curve continued to favour short- and intermediate-term over long-term.

Inflation & real assets: With headline inflation easing but services still firm, index-linked gilts sat alongside quality nominals. Precious metals were sized mainly for risk control; interest persisted in energy-transition exposures (e.g., copper, grid/data-centre infrastructure) via diversified vehicles.

What could move markets in Q1 2026

Central banks: Early-quarter meetings will shape how fast the US eases and how long the UK/Euro area stays on hold.

Earnings breadth: Do gains continue to spread beyond the mega-caps, especially outside the US?

Rates & liquidity: Long-end gilts and balance-sheet policy remain wild cards; the US curve stayed steeper into year-end.

Commodities & FX: Precious-metals momentum and the dollar’s path are steering EM risk appetite.

Key dates (subject to change)

UK - Bank of England (MPC): 5th Feb & 19th Mar • Dec CPI (21st Jan), Jan CPI (18th Feb) & Feb CPI (25th Mar)

US - Federal Reserve (FOMC): 27-28 Jan & 17-18 Mar • CPI Jan (11th Feb) & Feb (11th Mar)

Euro area - ECB: 4-5 Feb & 18-19 Mar • HICP: flash early-month Jan (4th Feb), Feb (3rd Mar) & Mar (31st Mar); final mid-month Jan (25th Feb), Feb (18th Mar)

Quarterly performance statistics

UK:FTSE All-Share +33.2% in 2025 (USD terms).Q4: UK equities rose +6.3%; leadership from globally exposed large-caps (financials, mining, defence). Gilts outperformed major peers.

US:S&P 500 +17.9% for 2025.Q4: Equities gained +2.7%; late-December wobble looked like profit-taking. Leadership stayed concentrated in comms/tech while industrials, financials, healthcare, and utilities posted double-digit full-year gains. Fed −25 bps in Oct & Dec.

Europe ex-UK:MSCI EMU >40% in 2025 (USD).Q4: Eurozone shares delivered positive performance +5.1%; financials led; defensives attracted interest as yields fell; ECB on hold in December; 2025 growth projection raised to 1.4%.

EM/Asia:MSCI AC Asia ex-Japan +4.3% in Q4; +32.3% in 2025 (USD).Korea/Taiwan led; China softer late Q4. Japan:Q4 (local): TOPIX Total Return +8.8%; Nikkei 225 +12.0%.

Bonds:Q4:UK gilts outperformed; BoE −25 bps (5–4) in December; US curve steepened; EUR/GBP investment-grade credit posted positive total returns.

Commodities:2025:Gold >60% (Q4 +12%), silver >140% (Q4 +54%); WTI US$57/bbl at year-end (near 20% y/y decline).

Bottom line

Cooling inflation, gentle policy support, and resilient earnings met a market that was starting to broaden beyond US mega-caps. For diversified investors, that tends to argue for breadth over bravado, quality over conjecture, and risk controls left firmly on.

How Oakcrest helps

We don’t believe in forecasting headlines; we focus on building portfolios and plans that can adapt as conditions change.

If you’d like to sense-check your current positioning, or discuss how today’s market backdrop fits within your wider family, trust or business plans, we’d be pleased to have a conversation.

Thanks for reading,

Oakcrest Private Office

The content in this article was correct on 09/03/2026.